The Federal Budget announced by the Labour Government on 25th October ended up more like a Mid-Year Fiscal Update with very few surprises or tax changes. As expected, the government gave a wide berth to any potential tax reform measures in this budget but that confirms that more significant changes to fiscal policy is expected in the next Budget to be announced on 9 May 2023.

The Budget Update did announce measures to assist with cost of living pressures in the form of:

- Paid Parental Leave (PPL) scheme — proposed expanded access to the PPL scheme, although these changes will be progressively implemented from 1 July 2024 to 1 July 2026.

- Cheaper childcare — a proposed increase in the Child Care Subsidy rate from 1 July 2023.

- Downsizer contributions — a proposed reduction in the eligible age for making downsizer contributions from 60 to 55 to provide greater flexibility to contribute to superannuation, support eligible taxpayers to downsize sooner and increase the availability of suitable housing for families (effective from the start of the first quarter after the enabling legislation is enacted – hopefully 1 January 2023).

- Changes for pensioners — a proposed extension in the assets test exemption for sale proceeds of the principal home from 12 months to 24 months as well as changes to the income test (giving pensioners more time to purchase replacement homes).

- COVID-19 business grants — treating a range of COVID-19 state and territory government support payments made to businesses in Victoria and the ACT as non-assessable non-exempt income (tax free).

The Budget Update also confirmed that they would not be proceeding with proposed changes that would have:

- Replaced the annual audit requirement for certain SMSFs with a three-yearly requirement; and

- Introduced a $10,000 limit for cash payments to businesses for goods and services

The budget also confirmed that proposed changes to relax the residency requirements for SMSFs will proceed which will allow greater flexibility for SMSFs with members living overseas but the commencement dates will be deferred.

We note that the Budget also confirmed funding for the ATO’s:

- Tax Avoidance Taskforce (targeting mostly high wealth private groups particularly in relation to international & trust transactions);

- Shadow Economy Program (eg expansion of Taxable Payments Reporting System);

- Personal Income Tax Compliance Program (re undeclared income & overclaimed expenses); and

- Modernising Business Registers program which will consolidate over 30 business registers on to one platform.

So, making sure you keep appropriate records and comply with the Tax Legislation is important.

As it turns out, what it didn’t say is more interesting than what it did say:

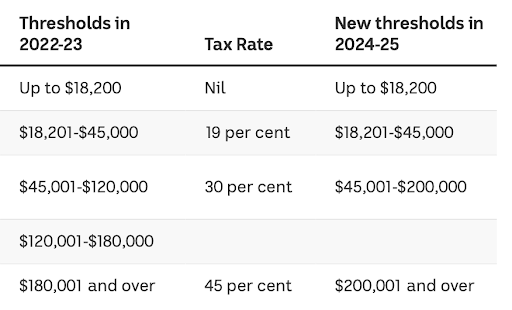

There were no changes to the Liberal Government’s Stage 3 Tax Cuts due to come into effect from 1 July 2023. So, the tax thresholds for the next few years look like:

There were many previously announced but unenacted measures that have been left in limbo. These include proposed changes re:

- Changes to Individual & corporate residency for tax purposes;

- Deductions for education & training expenses for individuals;

- Reforms to Division 7A (company loans to associated people);

- Clarification of Non-arm’s length income (NALI) for SMSFs; and

- Reduction of FBT record keeping requirements.

There is also a lot of other legislation currently still in draft form:

- Electric Car FBT exemption – proposed to start 1 July 2022. It is currently before the Senate. It is a step towards the tax system being engaged as a primary mechanism to deliver incentives and encourage behavioural changes to address climate change.

- Commonwealth Seniors Health Card income test threshold – Once the legislation receives Royal Assent the threshold will be increased to:

- $90,000 for singles (up from $57,761); and

- $144,000 for couples (up from $92,416).

- Removal of the $250 non-deductible threshold for self-education expenses from 1 July 2022.

- 120% Deduction for External Training Expenditure on employees by RTO’s – for businesses with under $50M turnover. Proposed to take effect 7.30pm 29 March 2022 to 30 June 2024 but since not law yet businesses will need to claim any 2022 expenditure in their 2023 tax return.

- 120% Deduction for Digital Take-Up Expenditure for businesses with under $50M turnover. Proposed to take effect 7.30pm 29 March 2022 to 30 June 2023 but since not law yet businesses will need to claim any 2022 expenditure in their 2023 tax return. Note there is a cap on the amount of this bonus deduction each financial year of $20,000.

It is also worth noting that the Transfer Balance Cap (the maximum amount you can start a super pension with) is currently $1.7M. This cap gets indexed to inflation in $100,000 increments so it is possible that because it just missed out on getting indexed last year and with inflation running high this year that it might actually jump to $1.9M by 1 July 2023. This may be an important consideration for people wanting to start pensions in the next year or two.

The variety of new tax measures proposed to take effect and some retrospectively means it is important to stay in touch with your accountant to keep up to date with issues affecting your business and personal tax position. Please give us a call if you would like to discuss anything in more detail.